Common Misunderstandings Regarding Supplemental Insurance

- Christopher Sakamoto

- Mar 19

- 2 min read

Supplemental insurance is a frequent source of confusion because it doesn't work like your "main" health insurance. People often buy it thinking it’s a safety net, only to be surprised by how and when it actually pays out.

Here are the most common misunderstandings regarding supplemental insurance.

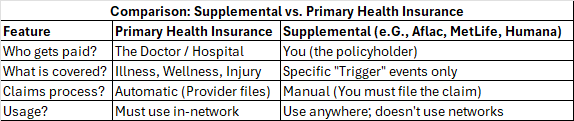

1. Misconception: It Pays the Doctor Directly

The Reality: Unlike your primary health insurance (which pays the hospital or doctor), most supplemental plans—like Accident, Cancer, or Critical Illness insurance—pay a cash benefit directly to you.

Why it matters: The supplemental insurance company sends you a check, and you decide whether to use it for medical bills, your mortgage, groceries, or childcare while you're recovering.

2. Misconception: "Supplemental" is the same as "Secondary"

The Reality: These are two very different legal structures.

Secondary Insurance: This is a second full health plan (e.g., being on your own employer's plan and your spouse's). They coordinate benefits to cover the same bill.

Supplemental Insurance: This is an "add-on." It doesn't coordinate with your primary plan; it simply triggers a payout based on a specific event (like a broken leg or a hospital stay).

3. Misconception: It Covers "Wear and Tear"

The Reality: Supplemental accident plans almost always require a defined event with a timestamp.

The Difference: If you develop carpal tunnel syndrome from 10 years of typing, an accident policy will likely deny the claim. If you trip over a power cord and break your wrist today, they will approve it. It must be a "sudden and unforeseen" accident, not a chronic condition.

4. Misconception: All Medicare Supplements (Medigap) are Different

The Reality: This is a unique case where the plans are actually standardized by the government.

If you are looking at "Plan G" from three different companies, the medical coverage is identical by law.

The Trap: People often choose the company with the lowest current premium, not realizing that some companies have a history of aggressive rate increases as you age. You aren't paying for better coverage; you’re paying for better customer service or more stable long-term pricing.

5. Misconception: It’s a "Replacement" for Health Insurance

The Reality: Supplemental insurance is not medical insurance.

If you only have a supplemental "Hospital Indemnity" or "Accident" plan and no major medical insurance, you are effectively uninsured for routine care, prescriptions, and specialists. These plans are "gap fillers," not a foundation.

Comments